Ready To Get Started?

Reach Out & Give Us A Call. We're Here To Help.

1800102111

Need Support?

Have Queries About Your Current Product? Please Write Us An Email & We'll Sort it Out.

customer.care@sbigeneral.in

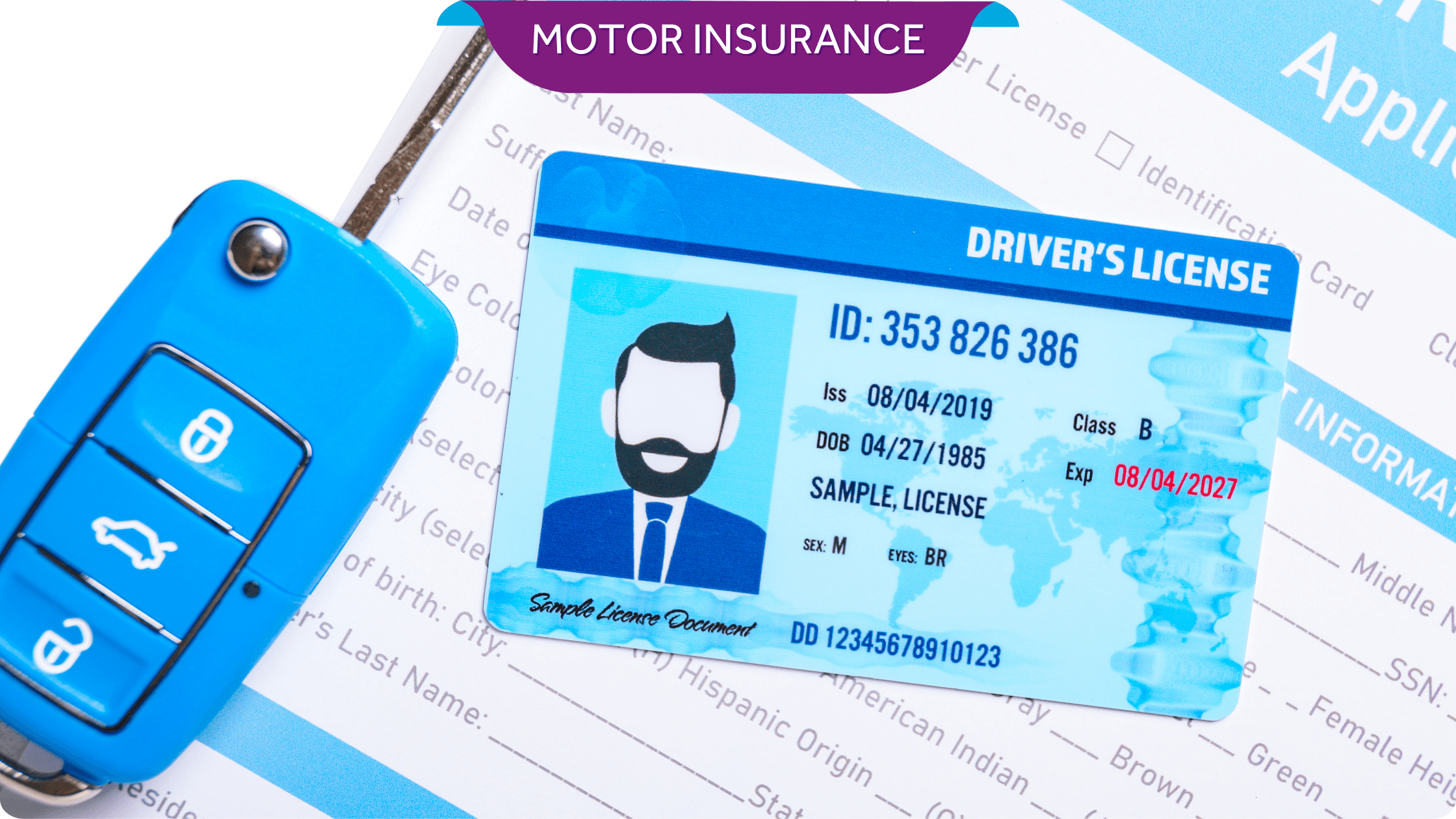

Insurance Alert: A Fake Driver’s Licence Can Cancel Your Claim

Imagine this: you’ve been involved in a minor car accident, and while you’re relieved no one is injured, your car requires significant repairs. You file a claim with your car insurance company, confident that your coverage will handle the costs. However, to your dismay, the claim is rejected—not because of the accident itself but because the driver at the time had a fake driving licence.

This scenario, while alarming, is not uncommon. In India, fake driving licences are a serious issue, and their implications can be far-reaching. Car insurance companies are increasingly scrutinising the validity of licences when processing claims. Here’s a comprehensive look at how this affects you and how to safeguard against it.

Why Do Car Insurance Companies Reject Claims for Fake Driving Licences?

Car insurance companies must ensure that claims are legitimate and comply with legal requirements. A fake driving licence violates the conditions of most insurance policies, as it indicates the driver was not authorised to operate the vehicle.

Key Reasons for Rejection

Violation of Policy Terms: Insurance policies typically require that the driver holds a valid licence. A fake licence breaches this condition.

Legal Implications: Driving with a fake licence is illegal, which can void your car insurance coverage under the Motor Vehicles Act.

Risk Assessment: A fake licence undermines the insurer’s ability to evaluate the risk accurately, leading to claim denial.

How to Detect a Fake Driving Licence

Identifying a fake driving licence can be challenging, but there are key signs to watch for:

Check for Spelling Errors: Fake licences often have typos or formatting inconsistencies.

Verify with the RTO: The Regional Transport Office can confirm the authenticity of a licence.

Digital Verification: Use online government portals to cross-check licence details.

Consequences of Using a Fake Driving Licence

Driving with a fake licence has serious repercussions for drivers and vehicle owners.

Legal Actions: Attempting fraudulent claims or using counterfeit policies can result in severe legal penalties, including fines, imprisonment, and a criminal record. Legal proceedings can be both time-consuming and costly.

Financial Losses: Victims of fake insurance policies may find themselves unprotected in emergencies, leading to significant out-of-pocket expenses for vehicle repairs or replacements. Additionally, claims made under invalid policies are outright rejected by insurers.

Damage to Reputation: Involving in insurance fraud can tarnish an individual’s reputation, affecting personal and professional relationships.

Higher Premiums for All: Insurance companies often compensate for the losses incurred due to fraudulent activities by increasing premiums for all policyholders, affecting honest customers.

By recognising these risks and staying vigilant, you can protect yourself and contribute to a fairer insurance ecosystem.

Steps to Avoid Issues with Car Insurance Claims

Conclusion

Car insurance is a vital safety net, but its effectiveness depends on compliance with legal requirements. A fake driving licence can lead to claim rejection and expose you to legal troubles and financial losses. Ensuring the authenticity of a driving licence is a small but crucial step to protect yourself and your policy.

SBI General offers dependable car insurance solutions focusing on transparency and customer satisfaction. With their online platform, you can easily purchase and manage your policy while enjoying comprehensive coverage. By choosing SBI General, you ensure a hassle-free insurance experience prioritising your safety and peace of mind.

Frequently Asked Questions

Recent Blogs

Motor Insurance

Real-life situations where you need motor insurance

- Your car is damaged in a collision with another car

- Collision insurance will compensate you for the cost of repairing damage to your car, provided your deductible is lower than the total repair cost

- You injure another driver and/or damage his car in a collision

- Third-party motor liability insurance covers you from legal liability for injury or property damage to another person due to an accident in which you were involved. This also covers compensation claims by their family after death.

- Your car is involved in a collision with another car and you suffer injury

- Personal Accident cover gives protection to both the owner-driver and a hired driver for death or injury in a motor accident (100% claim is awarded in case of death/severe limb damage).

- Your car is involved in a collision with another car and the other driver is injured

- Bodily Injury Liability Insurance will cover the other driver's treatment costs if they don't have Personal Accident insurance themselves.

- Your car is stolen from your office parking-lot / destroyed in a collision

- Your insurer will compensate you for the depreciated cost of your vehicle at the time of the crash. If you have the Return to Invoice add-on, you could instead get compensated for the full sticker-price of the car, as new.

- Your car’s engine or electronic circuit are damaged by floods

- The Engine Guard add-on compensates you for damage suffered to the engine and circuits, e.g. hydrostatic lock during floods (NB: it’s meant for unforeseen failures, not wear-and-tear repairs).

- You suffer an accident or serious breakdown on a remote highway

- A roadside assistance add-on lets you call for help when driving through a remote area. This covers everything from punctures to battery failures. You will usually get fuel, transport and short-term accommodation in the area.

- Your mobile phone and laptop are stolen from your car

- Insurance add-ons compensate customers for theft of belongings from a locked car. A wide range of covers is available, up to as much as Rs. 50,000.

- You are stuck without a car as your car is being repaired after an accident

- The Daily Allowance add-on reimburses you for the expense of finding alternative transport if your car is damaged/stolen. The amount could be as much as Rs. 1,000 per day, for up to two weeks.

Motor Insurance

Can I Ride My Bike Without Insurance?

Driving vehicles, especially two-wheelers, in a densely-populated country like India can be quite challenging. With bumper-to-bumper traffic and people breaking rules willy-nilly, travelling without insurance is like inviting trouble. It is thus essential to take precautions since accidents can impact you physically, legally, and financially. One way to secure yourself is to invest in bike insurance. Insurance companies compensate your for losses and damages when your two-wheeler is involved in accidents. If you are wondering – can I ride a motorcycle without insurance, this article provides the answer.

What happens when you ride a motorcycle without insurance?

You could face the following consequences if you ride your bike without a valid and active two-wheeler insurance plan:

Legal action:

Riding your bike without insurance is a punishable offence in India, which can lead to various legal consequences. If a traffic authority catches you driving without valid insurance, you could be fined or imprisoned for up to three months, or both, under the new Motor Vehicles Act, 2019. If you are deemed guilty of this offence a second time, authorities may increase the fine amount.

Denial of claim request:

You cannot claim damages sustained by your vehicle if you venture on a bike ride without insurance. Insurers do not entertain your claim since they would deem you guilty of violating Indian traffic laws.

Loss of no claim bonus:

Buying insurance is not enough. You have to renew your insurance plan every year and ensure you are always eligible for coverage. If you fail to renew the policy and keep it active, you stand to lose the accumulated no-claims bonus.

Possibility of inspection:

Since driving without inspection is against the laws, you would have to eventually renew or purchase a new insurance plan altogether. In such cases, you would need to give your vehicle for inspection, which can be quite the hassle.

Pay for third-party damage:

If you ride your bike without valid bike insurance, you would also be required to fulfil any third-party liabilities in case you cause damage to third-parties or their vehicle/property. You would have to compensate them for repairs, physical injuries, etc., from your pockets.

Paying fines for riding a motorcycle without insurance

Paying the applicable fine is an immediate consequence of riding your bike without your insurance policy. You can pay the fine offline or online. The offline process involves visiting your nearest traffic police station. In the online method, you can visit the official website of the state transport department, select the e-challan payment section, enter the challan number, and make the payment.

Get bike insurance

Now that you have the answer to the question – can I ride a bike without insurance, you can make the right choice. You must get bike insurance to avoid the penalties and stay financially protected from unexpected mishaps. Typically, you should buy the policy soon after you purchase your two-wheeler. You should also renew it annually to enjoy continuous coverage. You can buy the plans online and offline. Once you get the bike insurance documents, you must carry them with you whenever you ride your bike.

Disclaimer: The above information is indicative in nature. For more details on the risk factor, terms and conditions, please refer to the Sales Brochure and Policy Wordings carefully before concluding a sale.

Motor Insurance

Learn About Car Insurance Claims During Different Situations

Whether you buy car insurance online or offline, it's a pivotal aspect of retaining a vehicle. It allows you to stay financially ready to face any events like natural disasters, fire, accidents, and more, where your vehicle may be involved. While we hope to not witness these situations, it is essential to understand how car insurance claims work and the methods involved in the process of third-party insurance claims. The protection offered by car insurance can be categorised into two types – third-party and own damage. Comprehensive insurance claims are subject to terms and conditions set forth under the car insurance claim policy.

Types of Car Insurance Claims

Car insurance claims can be broadly categorised into two categories based on the insurance coverage you are claiming. Here is a list of them:

- Third-Party Insurance Claims

- Own Damage Insurance Claims

When you're involved in an accident that causes damage or injury to someone’s property or person, you may need to make third-party insurance claims. In similar cases, your insurance company will handle the legal and monetary aspects of the claim on your behalf. This includes compensation for the other party's medical costs, vehicle restoration, or all legal charges incurred. Claims are subject to terms and conditions set forth under own damage insurance.

Own damage claims cover the costs of repairing or replacing your vehicle in the event of an accident, theft, fire, or natural disaster. To be suitable to make this claim, you need to have Own Damage insurance that comes with a comprehensive insurance plan.

Making Car Insurance Claims – Steps to Follow

Knowing how to make a car insurance claim is important. Here is a step-by-step guide that helps to understand how comprehensive insurance claims can be made in a structured process:-

- Notify the Insurance Company

- Gather Necessary Information

- Submit a Claim Form

To start making a car insurance claim, inform your insurance company as soon as possible. Utmost insurance providers have a specific time frame within which claims must be reported. Failing to notify the insurer instantly may cause a rejection of your claim.

When starting a claim, you may be required to give primary information like policy number, mishap details, etc. All this data should be well-prepared.

Your insurance company will give you a claim form to fill out. This form will allow you to give essential details about the incident and the extent of the damage or injuries involved. Be thorough and accurate when completing the form.

When Making Third-Party Insurance Claims

- Exchange Information

- Provide Witness Statements

- Cooperate with the Insurance Company

Exchange contact and insurance details with the other party involved in the incident. This includes their name, contact number, insurance company, and policy number.

Request witnesses to support their own damage insurance claim if possible.

Follow instructions given by the insurance company and give as much information as possible to make the claim settlement procedure easy.

When Making Own Damage Insurance Claims

Follow these steps when making your own damage insurance claims for car insurance

- Get Your Vehicle Assessed

- Obtain Repair Estimates

- Maintain Documentation

Communicate to your insurance company to arrange for an assessment of the damage. They may ask a representative to check your vehicle or direct you to an authorised centre.

Get repair gauges from approved carports or workshops. Yield these gauges to your car insurance provider for audit and endorsement before continuing with the repairs.

Keep all receipts, solicitations, and communication related to the repairs. These archives will be vital when submitting your claim for damage payment.

When Making Comprehensive Insurance Claims

- Inform your insurance company

- Register an FIR

- Take photos and videos

- Submit documents

- Get your car inspected

- Wait for the claim settlement

Frequently Asked Questions

- How can I buy car insurance online?

- Do I need to write a car insurance claim letter?

- How much time will my car insurance claim processing take?

To purchase car insurance online, visit the websites of different insurance suppliers. Fill in the required subtle elements, compare cites, and select the approach that suits your needs. Make the instalment online to total the purchase.

In most cases, a claim form handed in by your insurance company suffices. Still, in certain situations, similar to complex claims or disputes, a written claim letter for car insurance may be needed. Claims are subject to terms and conditions set forth under the car insurance policy.

The time taken to handle a car insurance claim can shift depending on a few components, including the complexity of the claim and the responsiveness of the included parties. To get an assessed time based on your case, you may counsel your insurance supplier straightforwardly. Claims are subject to terms and conditions set forward beneath the car insurance arrangement.

Disclaimer: The above information is indicative in nature. For more details on the risk factor, terms and conditions, please refer to the Sales Brochure and Policy Wordings carefully before concluding a sale.

Motor Insurance

Insurance Alert: A Fake Driver’s Licence Can Cancel Your Claim

Imagine this: you’ve been involved in a minor car accident, and while you’re relieved no one is injured, your car requires significant repairs. You file a claim with your car insurance company, confident that your coverage will handle the costs. However, to your dismay, the claim is rejected—not because of the accident itself but because the driver at the time had a fake driving licence.

This scenario, while alarming, is not uncommon. In India, fake driving licences are a serious issue, and their implications can be far-reaching. Car insurance companies are increasingly scrutinising the validity of licences when processing claims. Here’s a comprehensive look at how this affects you and how to safeguard against it.

Access and manage all your Insurance Needs in one place, right at your Fingertips.

4.5/5*

Access and manage all your Insurance Needs in one place, right at your Fingertips.

Download Our App

We're socially active!